Use the News

By the USF Stavros Center in Collaboration with TBT NIE and FPES

|

|

|

|

With generous funding from State Farm

|

|

|

|

|

|

|

With generous funding from State Farm

|

|

Go to Nearpod.com. The link for today is CLWQE

Use the editable link to download into your Nearpod library. You can also download a copy or view below.

Please fill in the evaluation form

Check out resources in the Wakelet!

Did you know that the word "Benjamins" is slang for money? Check out the All About the Benjamins supplement from the Tampa Bay Times to learn more about money.

Benjamin Franklin was a great believer in thrift. In fact, from 1732-1758, he created a publication Poor Richard's Almanac(k) - written under the pseudonym of "Poor Richard" or "Richard Saunders." Saving is difficult. We have unlimited wants and have to make decisions about saving vs. spending. In order to understand the basics of saving, check out Practical Money Skills and try their Saving for a Goal calculator. After you have learned the basics, use the NIE Supplement All About the Benjamins to gather ideas to use in a social media post about thrift. For example, you can create an instagram or twitter post about thrift. Or you can create a short video public service announcement or an infographic.

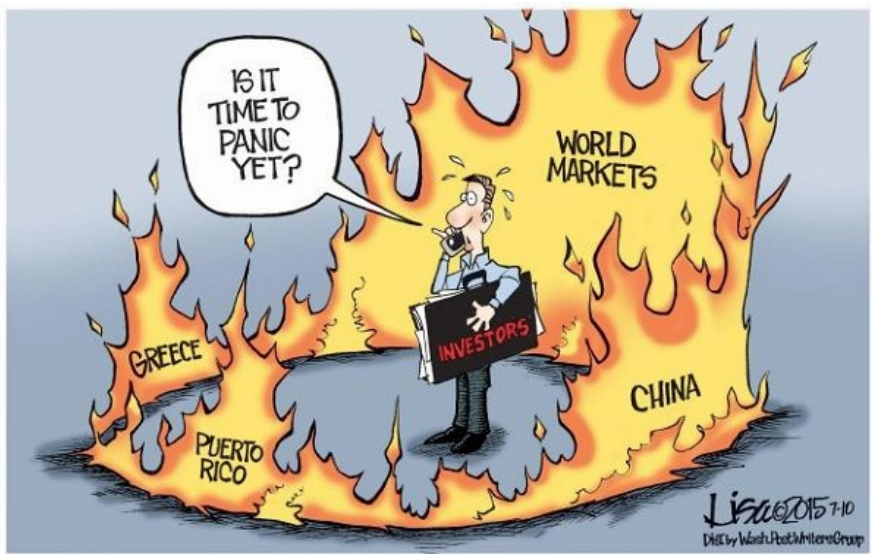

Standards SS.8.FL.3.7 Discuss the different reasons that people save money, including large purchases (such as higher education, autos, and homes), retirement, and unexpected events. Discuss how people’s tastes and preferences influence their choice of how much to save and for what to save. SS.912.FL.3.1:Discuss the reasons why some people have a tendency to be impatient and choose immediate spending over saving for the future.  This political cartoon was created in 2016 and made available from from the NIE and Association for American Editorial Cartoonists (AAEC) Cartoons in the Classroom program to discuss the stock market. Check out the information in the pdf of the political cartoon to describe describe how the stock market may adjust to news of panic in world markets. That was then and this is now. What are some world events that have caused shifts in the stock market in the past? What about the present? Choose an event and create your own cartoon or meme about the event. Financial Literacy Standard SS.912.FL.5.7:Describe how financial markets adjust to new financial news and that prices in those markets reflect what is known about financial assets.  In the past, there were many jobs for people who didn't know how to use computers. Today, most jobs require digital literacy. Many workers have gone back to school to take computer and other technology classes. The ability to understand coding is essential for many jobs of today and tomorrow. What technology skills do you have? What technology skills do you need? Check out the Newspaper In Education supplement from the Tampa Bay Times: Exploring Creativity Through Mobile App Development. Think of a problem you have. What kind of app could you develop to solve the problem?

Standards

SS.8.FL.1.2 Identify the many decisions people must make over a lifetime about their education, jobs, and careers that affect their incomes and job opportunities. SS.8.FL.1.3 Explain that getting more education and learning new job skills can increase a person’s human capital and productivity. SS.8.FL.1.4 Examine the fact that people with less education and fewer job skills tend to earn lower incomes than people with more education and greater job skills. SS.912.FL.1.3: Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. SS.912.FL.1.4: Analyze the reasons why the wage or salary paid to workers in jobs is usually determined by the labor market and that businesses are generally willing to pay more productive workers higher wages or salaries than less productive workers. SS.912.FL.1.5: Discuss reasons why changes in economic conditions or the labor market can cause changes in a worker’s income or may cause unemployment.

Watch this NIE video of the week on smoking bans. What do you think about the smoking bans? Why are some people willing to smoke and accept the risk? Why are people willing to pay for health insurance if they can avoid a larger loss later, especially if they participate in risky behaviors? Should smokers pay more for health insurance? Why or why not?

What about life insurance? Download the Life Insurance article below. How much more would a smoker pay than a healthy 30-year old woman for a $1 million policy with a 20-year-term? A healthy 30-year old man? A 45-year old woman for a $500,000 policy with a 30-year-term? How much more for a male smoker? What advice would you give to a male smoker who wants to lower his insurance premiums?

Financial Standards

SS.912.FL.6.1:Describe how individuals vary with respect to willingness to accept risk and why most people are willing to pay a small cost now if it means they can avoid a possible larger loss later. SS.912.FL.6.6:Explain that people can lower insurance premiums by behaving in ways that show they pose a lower risk.  “Hello Summer School, Goodbye Wages” Check out the student guide you can use and download for this lesson on making decisions about decision-making and informed career choices.

What did your last summer look like? A break from classes with a summer job, or more of the same? Did you have any say in what you did, or did parents make the decision for you? Did you perform a “cost benefit analysis” to determine what the best arrangement was for your future? If the proof is in the pudding, statistics show students around the country have concluded that skipping experience with work just makes sense; if that time is replaced with academics. The chance to get ahead in studies, or remediate when needed seems to be an increasing trend among high school teens. While students may be equipping themselves for college with extra studying, there is concern with a lack of work experience when entering the workplace. When high school students make the decision to forego working a part time job, what are they really giving up other than earning minimum wages? Discuss with a partner and make a list of what teens are sacrificing when they give up work experience. Read the article attached and consider the following:

Create a half page flyer, to help students in your career navigate between choosing summer school or summer work. You may choose to include a pro and con list, or a venn-diagram to help illustrate your thoughts.

Florida Financial Literacy Standards: SS.912.FL.6.9: Explain that loss of assets, wealth, and future opportunities can occur if an individual’s personal information is obtained by others through identity theft and then used fraudulently, and that by managing their personal information and choosing the environment in which it is revealed, individuals can accept, reduce, and insure against the risk of loss due to identity theft. SS.912.FL.1.1: Discuss that people choose jobs or careers for which they are qualified based on non-income factors, such as job satisfaction, independence, risk, family, or location. SS.912.FL.1.2: Explain that people vary in their willingness to obtain more education or training because these decisions involve incurring immediate costs to obtain possible future benefits. Describe how discounting the future benefits of education and training may lead some people to pass up potentially high rates of return that more education and training may offer. SS.912.FL.1.3: Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. SS.912.FL.1.4: Analyze the reasons why the wage or salary paid to workers in jobs is usually determined by the labor market and that businesses are generally willing to pay more productive workers higher wages or salaries than less productive workers. Literacy Standards LAFS.K12.R.1.1 Read closely to determine what the text says explicitly and to make logical inferences from it; cite specific textual evidence when writing or speaking to support conclusions drawn from the text. LAFS.K12.W.3.8 Gather relevant information from multiple print and digital sources, assess the credibility and accuracy of each source, and integrate the information while avoiding plagiarism.  Check out the student guide that accompanies this post:

When job hunting, teens eager for their first job, are quick to take what is offered- anything to get that first paycheck. Likewise, soon out of college, young adults intent on pinning down a professional job to make use of their college degree and pay off that school debt, will take the first job that comes their way. Fearful of letting any opportunity be a missed opportunity, many adults are not taking their time to truly evaluate job offers that come their way. Many career opportunities present themselves with a variety of benefits that exceed the paycheck. Fringe benefits like a company car, health insurance, travel per diem, access to a gym or even discounts with phone companies are common in attempt to not only lure quality workers but retain them. Studies show that 30% of individuals do not know if their employer provides the benefits of a retirement plan. Employers are only 70% of the way to clear communication regarding financial or retirement benefits with their workers. Is it the job of the company to furnish ample information to educate their wage earner regarding fringe benefits and retirement plans? Absolutely! However, it would be remiss to not hold the laborer responsible as well. When offered a job opportunity, do not miss out on considering fringe benefits as payment too! Employees at any age should take charge of their retirement future, near or far, and investigate what is best for them. Putting money aside from every paycheck, paying yourself first is the way to get ahead. Read the attached article.

Why do you think that 30% of those surveyed do not know what benefits their employer offers? Does this surprise you? Why or why not? What benefits are important to you? Make a list of benefits that would lure you away from one employer to another. Use Fidelity’s article to think about how much money you should reserve from your monthly paycheck for retirement.

Conduct more research on fringe benefits offered by employers. Design a half page flyer to educate college students on what to research when considering fringe benefits. On the back of the flyer, explain how a 401K works. Florida Financial Literacy Standards: SS.912.FL.1.1: Discuss that people choose jobs or careers for which they are qualified based on non-income factors, such as job satisfaction, independence, risk, family, or location. SS.912.FL.1.3: Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. SS.912.FL.3.7: Explain how employer benefit programs create incentives and disincentives to save and how an employee’s decision to save can depend on how the alternatives are presented by the employer. SS.912.FL.6.3: Describe why people choose different amounts of insurance coverage based on their willingness to accept risk, as well as their occupation, lifestyle, age, financial profile, and the price of insurance. Literacy Standards LAFS.K12.R.1.1 Read closely to determine what the text says explicitly and to make logical inferences from it; cite specific textual evidence when writing or speaking to support conclusions drawn from the text. LAFS.K12.W.3.8 Gather relevant information from multiple print and digital sources, assess the credibility and accuracy of each source, and integrate the information while avoiding plagiarism.  Here is the student guide that goes with this activity.

During the current COVID-19 shut-downs, many people have either lost their jobs or are working from home. Some workers have been deemed essential. Take for example, the healthcare workers, who are tirelessly helping people who have fallen victim to the virus. Now, check out the recent article from the Tampa Bay Times on essential workers. Before Reading: Consider the title: Cities differ on who's essential, who's not. Why do you think cities might differ in their assessments of which workers are essential? Predict some of the city workers that you think are deemed essential during the COVID-19 shut-down. During Reading: While you read, record which workers are deemed essential. Take notes to compare and contrast Tampa, St. Pete, and Clearwater.

After Reading: Which workers were deemed essential? What were the differences and similarities among the cities? Why were some people given more money than others? What changes in the labor market created these changes in salary? Why do you think some people have lost jobs? What else did you learn? Extension: Many of the jobs that were deemed essential are people with skilled trades. There are many different jobs people can do that don't necessarily require a college degree. Many of these jobs require certifications or on-the-job training. Sometimes people just apply to college without a future job in mind. Check out the Career Cluster infographic to learn more about different jobs and careers. What did you find? Now, visit Florida Shines.org to plan your future. When you find some jobs that look interesting, visit ONetOnline.org to conduct research on job options. What skills are required? What education is required? Which jobs match things you like? How much can you make? Use the PACED decision-making model to evaluate different jobs. Choose four different alternatives. Evaluate those alternatives, based on criteria important to you.

Florida Standards:

Language Arts-

Financial Literacy- SS.8.FL.1.1 Explain that careers are based on working at jobs in the same occupation or profession for many years. Describe the different types of education and training required by various careers. SS.8.FL.1.2 Identify the many decisions people must make over a lifetime about their education, jobs, and careers that affect their incomes and job opportunities. SS.912.FL.1.3: Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. SS.912.FL.1.5: Discuss reasons why changes in economic conditions or the labor market can cause changes in a worker’s income or may cause unemployment.  In a world of online sources, it is sometimes difficult to distinguish the COVID-19 facts from the fake. Check out the student guide that you can use with the resources in this post.

Have you heard rumors about COVID-19 cures? Check out this news video of the week from Tampa Bay Times NIE. What happened when the U.S. Customs and Border Protection agents found counterfeit coronavirus test kits at the O'Hare International Airport? What happened? Why do people create and sell fake test kits? What is your opinion about what they did? Use (and download) the OREO opinion writing graphic organizer to plan an opinion piece.

Now, check out this Tampa Bay Times article on rumors and hoaxes that are spreading coronavirus fears.

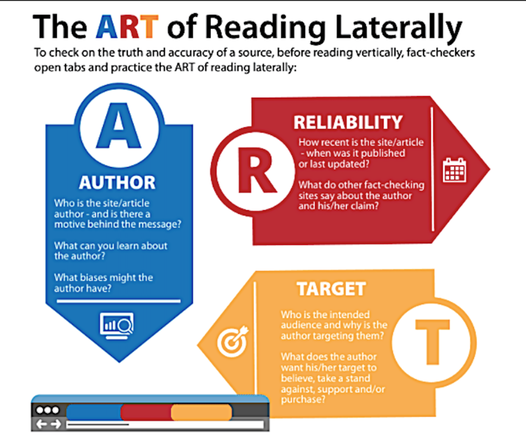

What do you think about some of the hoaxes? What are the possible consequences of these hoaxes spreading? How can you protect yourself from scammers who are trying to profit from the COVID-19 pandemic? Did you notice that the Tampa Bay Times turned to Politifact to determine facts from fake? At the bottom of this post, we included some other Fact Checking sites you can use. What are some reliable sources in these uncertain times? If you want to have the most current and reliable information, check: Then, check out this video by student reporters at CBC: What did you learn? Now, conduct some of your own research online. Use the strategy recommended by reporters and researchers: Lateral Literacy. Reading laterally means checking the truth and accuracy of the source (reading laterally) before reading the article (reading vertically). Find some article about COVID-19 online and use this when you are conducting your own research!  Record new facts you learned. Also, document some of the fake news that is out there. Now, create your own video, article, or social media post to warn people about fakes and teach them about the facts! Additional Free Fact Checking Sites:

Financial Literacy-

Check out our new blog post that discusses flattening the curve and provides an economic connection to COVID-19. Here is the student guide to view and download.

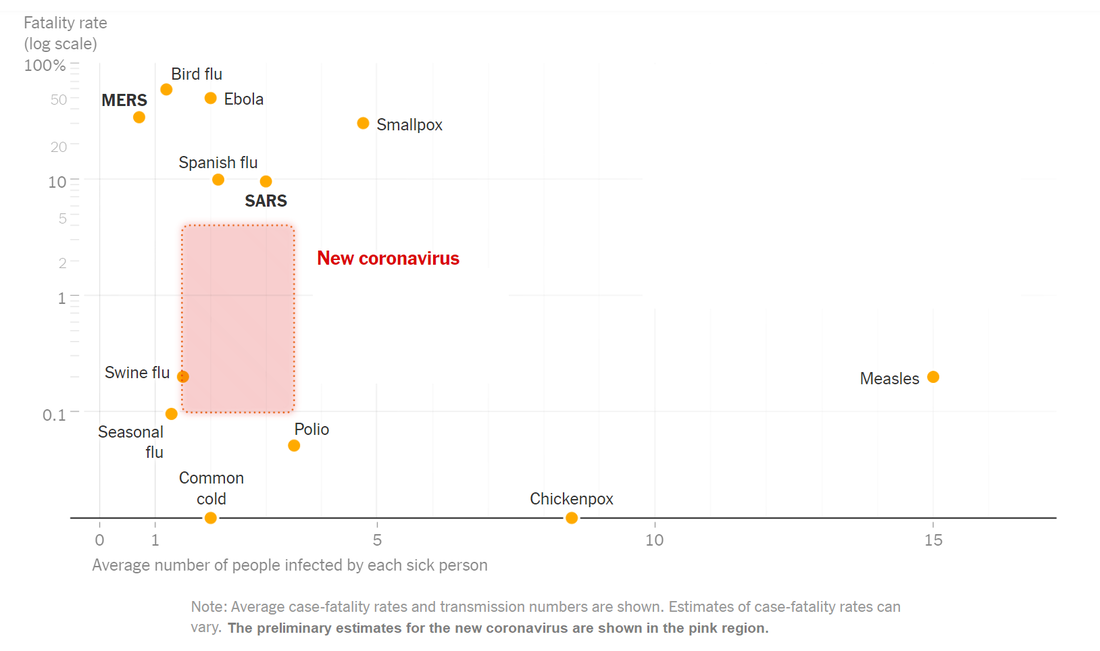

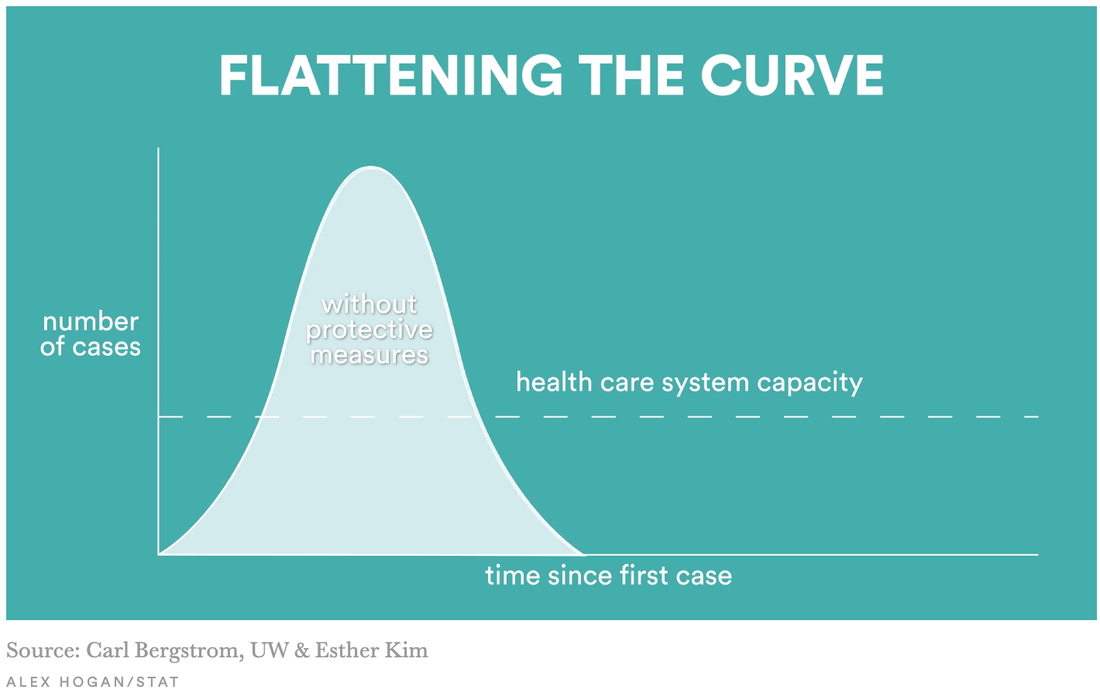

Riddle me this: What has the power to double in size every 3 days, yet it cannot be seen with the naked eye? Answer: SARS-CoV-2, the new strain of coronavirus. (COVID-19 refers to the disease that the new coronavirus (SARS-CoV-2) can cause; which broke out in 2019.) Riddle me this: What lock gives more and more freedom, the stronger the lock? Answer: A lockdown. The more people who participate in voluntary lockdowns (or “social distancing”) will provide a slower spread of disease and additional freedom from sickness. The slower the spread of any sickness, including the Coronavirus allows medical personnel to help those who need it most. Social distancing helps to “flatten the curve.” So, what does it mean to flatten the curve, and what does it have to do with economics? Remember the days of chickenpox? Or maybe your generation has received the vaccine shot to thwart this childhood illness that was once unhealthily considered a “rite of passage” to children until the mid 90’s. How different is this new strand of the Coronavirus to the old one, or to the common cold for that matter? Check out a quick graph from the New York Times to compare.  What surprises you about this chart? How familiar are you with these other infectious diseases? Does what you think you know match the data? Shouldn’t we all just keep to washing our hands and staying home if we are the ones who are sick- just as we did before this pandemic? What is the big deal? How and why do medical professionals want us to flatten the curve? What curve exactly? Reading through the article Coronavirus in Florida latest: Statewide closings, new cases, flattening the curve by Tampa Bay Times posted March 18, 2020, you can learn what is making some business owners and parents nervous as well as identify some economic issues at hand.

The end of the article hints at flattening the curve but doesn’t say how or what that infamous curve even is. If you have time, you can access their link to the suggested podcast, but you can also just keep reading here! Take a look at how Mydel Antolin explains “flattening the curve” on CBC’s Kids News. What does that curve look like if you had to draw it? How would you flatten that curve? Statnews provides an excellent video clip to show just what that flattened image would look like.  The best step-by-step guide on how to flatten the curve is a simulator provided by the Washington Post: “Why outbreaks like coronavirus spread exponentially, and how to “flatten the curve.” Author Harry Stevens is a graphics reporter who creates some pretty cool simulations to teach Washington Post readers just how effective “social distancing” really can be. Watch each of the four simulations and feel empowered to spread the news on just what flattening the curve is, and why all Americans should participate. Make an educated guess on where America is relative to these four simulations. What about China? What about France and Italy?

Extension: Create a political cartoon to teach younger students about flattening the curve or economic issues of the coronavirus. Florida Standards: Financial Literacy-

Do you know why the prince turned into a beast? He refused to help a senior citizen by giving her shelter for the night! How can you teach the Beast to be more charitable? Use the News! You can use these blog posts we created on cooking for charity, running for charity, and the SPCA hosting dog weddings for charity. These activities include articles from the Tampa Bay Times along with standards-based questions. Being charitable can mean giving of your time, talent, and treasures. How can you volunteer your time? What career can you choose where you can do something to create a better world? Can you save some money to donate to your favorite cause? Did you know that donations can be tax deductible? Use the following resources to conduct research so you can create a social media campaign on being charitable.

This clip offers a great opportunity to bring in civic participation and service learning projects as well! Here are some standards connections for this post!  Florida, what's not to love? Sand, sea and no state taxes! Image: Stock Photo Pixabay What do both professional athletes and retired citizens have in common? Well, if they live in Florida, they do not have to pay state income tax. But this fact is also true of anyone who lives in the state of Florida. Currently, the state of Florida has zero income tax. This means big bucks weigh more to athletes who make hundreds of thousands of dollars, and even millions. They get to keep more of their money. This is equally significant to senior citizens who have limited incomes or are existing on strict retirement incomes. Their money stretches farther than if they were to live in another state. Read or download the Tampa Bay Times article Florida a Strong Draw for Northerners Taxed to the Hilt.

Currently, nine states have zero income tax, Alaska, Florida, Nevada, South Dakota, Texas, Washington, New Hampshire and Tennessee. Those last two states, do tax investment income and interest. Moving north, just outside of the state of Florida to Alabama with 2-6% or Georgia at 1-6% state income tax, households pay a percent of their income to the state through annual state taxes.

Many people look for retirement in a warm and sunny spot to ease the aches and pains of getting older hoping to eschew battling heavy winters. They will also find Florida offers a respite for their finances while living on a fixed income. Why do you think forty one of our United States do have their residents file a state income tax? Why do you think that Florida does not have a state income tax? Do the research and look it up, why does the state not encumber their residents with a state income tax? If Florida did decide to tax its residents, what should the money be used for? Extension: Pen a letter to the Florida legislature (select a representative or senator who represents your town, of which you are a constituent) on your opinion of having a state tax. Be sure to support your ideas with at least three facts (always giving credit). When you share your opinion, provide how your household are (would be) affected. When writing to a member of Congress, ensure that you have titled your letter appropriately, you may need to look up the correct way to address your intended. Give an accurate return address and you may just receive a letter in return. Florida Literacy Standards: SS.912.FL.1.6: Explain that taxes are paid to federal, state, and local governments to fund government goods and services and transfer payments from government to individuals and that the major types of taxes are income taxes, payroll (Social Security) taxes, property taxes, and sales taxes. SS.912.FL.1.7: Discuss how people’s sources of income, amount of income, as well as the amount and type of spending affect the types and amounts of taxes paid.  Just like computers have cookies, Google has browser history and social media prompts you with ads based on your searches; your credit card company has you right where they want you! Credit card companies have software programs to track buying habits. Every time you swipe your credit card, data is collected by a company whose job is just that- to collect info about you. Information such as where you shop, what you purchase and how often. Companies are then able to establish consumer trends, on you specifically. They are able to sell this information, based on data and assumptions to businesses who want to market to you based on gender, age, political affiliation, hobbies, geographic location and other specifics. Brainstorm a list of details that companies would pay big money to find out about potential consumers. Read the article attached and take notes about the type of information that companies are looking for.

Analyze the list that you created and determine which pieces of information you would be willing to make public and which items you would rather keep private. At the end of the article, author Bluth gives the reader suggestions to keep your data from reaching these companies. Design a small card, like a business card, that adults and teens could keep in their wallets to remind them to be safe and smart consumers.

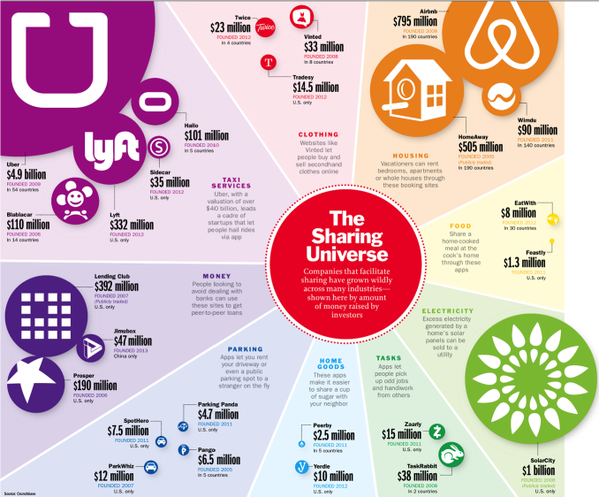

Florida Literacy Standards: SS.912.FL.2.2: Analyze situations in which when people consume goods and services, their consumption can have positive and negative effects on others. SS.912.FL.6.9: Explain that loss of assets, wealth, and future opportunities can occur if an individual’s personal information is obtained by others through identity theft and then used fraudulently, and that by managing their personal information and choosing the environment in which it is revealed, individuals can accept, reduce, and insure against the risk of loss due to identity theft.  New apps are available to split electronic money between parties. Gone are the days of bringing cash wherever you go. Instead of handing the dough over to friends or family when you owe, you can send them money virtually. Now, that is REAL money, but sent virtually. In the world of virtual reality, this idea has become reality. It is not the virtual that has become real, but that the real money can move virtually. What are the advantages of these apps? What people or groups may find these apps helpful? Are there concerns that the payer may have? What about concerns of the payee? Can you think of when the use of a P2P app is unacceptable? Users of apps such as Zelle or Venmo have found out that if they mistype a phone number or an email address, they will send their cold hard cash to a stranger, and may not get it back. Failure to send money to the correct person may mean that you lose that dollar amount and “repay” funds to the correct individual. Read the attached article to learn about the new peer-to-peer apps in the marketplace. After reading the article, research to see what the state of Florida has to say about the use of these type of “cash apps.” Create a guide to P2P payment apps for students. Include three sections:

Extension:

Use the graphic and articles to investigate how P2P apps are used fraudulently. Use the Better Business Bureau and Consumer Reports to compare and contrast two different peer to peer payment apps.

SS.912.FL.2.1: Compare consumer decisions as they are influenced by the price of a good or service, the price of alternatives, and the consumer’s income as well as his or her preferences. SS.912.FL.2.3: Discuss that when buying a good, consumers may consider various aspects of the product including the product’s features. Explain why for goods that last for a longer period of time, the consumer should consider the product’s durability and maintenance costs. SS.912.FL.2.5: Discuss ways people incur costs and realize benefits when searching for information related to their purchases of goods and services and describe how the amount of information people should gather depends on the benefits and costs of the information. SS.912.FL.2.7: Examine governments establishing laws and institutions to provide consumers with information about goods or services being purchased and to protect consumers from fraud. SS.912.FL.6.8: Discuss the fact that, in addition to privately purchased insurance, some government benefit programs provide a social safety net to protect individuals from economic hardship created by unexpected events. SS.912.FL.6.10: Compare federal and state regulations that provide some remedies and assistance for victims of identity theft.  Have you ever found it difficult to concentrate in school because you are worried about your grades? Although you are at school to make the effort to boost your grades, sometimes just being at school can cause your stress meter to skyrocket. Would it be more helpful if your courses in high school offered guidance on how to use your time to earn the best grade? Is this a part of your instructor’s responsibility? Well, many employees across the nation are experiencing the same stresses with their employers. A recent Yale study found that up to ten percent of workers may miss twenty one days due to work related stress. These lost work days impact the employer. Although this number does not account for days lost because of financial or psychological stress, employers watch aware as absenteeism continues to increase. Households across America worry about debt in an alarmingly increased rate. Employers offer pet insurance yet turn a blind eye to employee’s financial woes by neglecting to offer a place to turn for financial advice and help with student loans. Would money trouble affect your ability to be productive in the workplace? Why do you think some people have this struggle? Employers are becoming more and more progressive offering benefits millennials demand, like paternity leave, pet insurance and options for working at home, yet some fail to consider offering help where workers may need it the most… budgeting and debt elimination plans.

After reading the article, talk with a partner and answer the same questions under the conclude part of your chart.

Share your t-charts with the class and discuss your answers. Were there changes to your original opinion when you were speculating compared to your thoughts after reading the article? To conclude this learning activity, create an infographic that details at least 10 facts and 10 pictures that show the relationship between employers, employees, the workplace and financial health. Extension: Spend some time going through the following links to see why burned out workers are actually missing time at work. Come up with a warning list for employers including the top five things to look for in employee exhaustion. Write a letter to a CEO or local business owner sharing ways to support their employees with each of the five types of “burn out” you have selected.

SS.912.FL.1.5: Discuss reasons why changes in economic conditions or the labor market can cause changes in a worker’s income or may cause unemployment. SS.912.FL.4.8: Examine the fact that failure to repay a loan has significant consequences for borrowers such as negative entries on their credit report, repossession of property (collateral), garnishment of wages, and the inability to obtain loans in the future. SS.912.FL.4.9: Explain that consumers who have difficulty repaying debt can seek assistance through credit counseling services and by negotiating directly with creditors. SS.912.FL.4.10: Analyze the fact that, in extreme cases, bankruptcy may be an option for consumers who are unable to repay debt, and although bankruptcy provides some benefits, filing for bankruptcy also entails considerable costs, including having notice of the bankruptcy appear on a consumer’s credit report for up to 10 years.  Planning ahead is essential in all things financial. Many families are seeing great benefits planning ahead when it comes to college as well. Is this something to pay attention to? Planning for babies to go to college? Why would parents make a decision to pay for college in advance? We rarely order meals in advance, and never buy 10 -year-olds a car, so why would we buy a university experience for a baby? Prepaying for college has many advantages. Florida Prepaid College Program has just hit its 30th birthday and has helped almost 500,000 children make their college dreams come true. Read the article attached and think about the following: Why do parents make the decision to pre purchase college for their children? Does it make a difference? Support your conclusion. What could parents do instead of choosing to invest in college for their baby? Would you consider the FPCP an investment? Is it risky to participate in this program? Does the Florida Prepaid program mean that college students will not accrue student loan debt? What happens if the child fails to attend college? What impact would it have if double the parents participated in Florida Prepaid? Would this change the job market for college graduates?

Take your findings and write a letter to a parent of a newborn explaining the program, providing costs and benefits and conclude with an “advisement” to parents regarding their decision to participate in the Florida Prepaid program.

Extension: Create a short PowerPoint or Prezi to compare the cost of student loans with interest over time. Use the national average for student loan debt of $37,000. Investigate using the Florida Prepaid website how much it costs to invest in the program this year for a child born in January of 2019. Configure a chart to show how the same money grows over time in comparison to a bank savings account using the same dollar amount invested in FPCP. Add a slide to share what happens when graduates default on a student loan. What are the consequences if the loan is not repaid? What options are available specific to student debt? Related Standards SS.8.FL.2.1: Explain why when deciding what to buy, consumers may choose to gather information from a variety of sources. Describe how the quality and usefulness of information provided by sources can vary greatly from source to source. Explain that, while many sources provide valuable information, other sources provide information that is deliberately misleading. SS.8.FL.2.3: Describe the variety of payment methods people can use in order to buy goods and services. SS.8.FL.2.4: Examine choosing a payment method, by weighing the costs and benefits of the different payment options. SS.912.FL.3.1: Discuss the reasons why some people have a tendency to be impatient and choose immediate spending over saving for the future. SS.912.FL.3.3: Compare the difference between the nominal interest rate which tells savers how the dollar value of their savings or investments will grow, and the real interest rate which tells savers how the purchasing power of their savings or investments will grow. SS.912.FL.6.1: Describe how individuals vary with respect to their willingness to accept risk and why most people are willing to pay a small cost now if it means they can avoid a possible larger loss later. SS.912.FL.4.8: Examine the fact that failure to repay a loan has significant consequences for borrowers such as negative entries on their credit report, repossession of property (collateral), garnishment of wages, and the inability to obtain loans in the future. SS.912.FL.4.9: Explain that consumers who have difficulty repaying debt can seek assistance through credit counseling services and by negotiating directly with creditors. SS.912.FL.4.10: Analyze the fact that, in extreme cases, bankruptcy may be an option for consumers who are unable to repay debt, and although bankruptcy provides some benefits, filing for bankruptcy also entails considerable costs, including having notice of the bankruptcy appear on a consumer’s credit report for up to 10 years. SS.912.FL.5.10: Explain that people vary in their willingness to take risks because the willingness to take risks depends on factors such as personality, income, and family situation.  Check out the new student guide to use with this lesson!

What many new homeowners don’t know is that a mortgage is a whole lot more than a house payment. While owning a home can bring many assets, it comes with liabilities as well. A house payment is only for those who understand and know the responsibilities, financial and otherwise, that come with it. Many believe that the American Dream is to own a home. It is for over 50% of the American population, but many millennials have made the shift to renting. Home ownership much more complicated than making that monthly mortgage payment. What do you know about owning a home? What do you know about renting? Think of some advantages to owning your home. Make a list of positives and negatives that come with homeownership. Different people find different reasons to support getting in debt to achieve the American mortgage. Put a star by the two most advantageous to suit your personality. Mark a star next to the two most disadvantageous that make you wary of signing your name on a mortgage contract. Consumers need to be educated about any product that they want to purchase and what responsibilities are involved. Where can you look to find information about mortgages? What about the responsibilities of homeownership? Does the government want you to be a homeowner or a renter? Are there differences with insurance if you are a renter compared to an owner? When you read through the article 3 Things Change, write down what a potential homeowner needs to be aware of when opting to buy rather than rent.

What trends do you notice the article suggests “take over” the mind of a homeowner? Compare your list with the article. What can you add? Talk with a partner on how your lists compare.

Together as partners, create a “Thoughts for a Potential Home Owner” pamphlet. Come up with three different types of people, identifying them based on: income, personality, habits and goals. Draw or make an avatar replica of each imaginary person and come up with a short bio for each one. Identify your three personalities as “renter,” “home owner” and “on the fence.” Write a paragraph that will help your “on the fence” decision maker come to a conclusion. Be sure to list multiple advantages and disadvantages to both owning a home and renting. Then compile a list of eight things to consider about homeownership, whereby you demonstrate that you understand how owning a home affects other areas of your life. Present your pamphlet, personalities, biographies, and thoughts to consider. Let the rest of your class decide what your “on the fence” personality will do based upon the content you share and what you have learned as a class. Extension: Find a property online to rent, and one to buy. Create a plan for your Owner Avatar and your Renter Avatar. Describe the rental and buying process and what decisions are applicable for each home. Financial Literacy Standards SS.912.FL.2.1: Compare consumer decisions as they are influenced by the price of a good or service, the price of alternatives, and the consumer’s income as well as his or her preferences. SS.912.FL.2.2: Analyze situations in which when people consume goods and services, their consumption can have positive and negative effects on others. SS.912.FL.2.3: Discuss that when buying a good, consumers may consider various aspects of the product including the product’s features. Explain why for goods that last for a longer period of time, the consumer should consider the product’s durability and maintenance costs. SS.912.FL.5.2: Explain how the expenses of buying, selling, and holding financial assets decrease the rate of return from an investment. SS.912.FL.6.4 Explain that people may be required by governments or by certain types of contracts (e.g., home mortgages) to purchase some types of insurance. SS.912.FL.1.7 Discuss how peoples sources of income, amount of income, as well as the amount and type of spending affect the types and amounts of taxes paid.  Check out the student guide that you can use with this lesson and article.

When is the last time someone asked your advice, and then completely ignored it? That is what some financial planners cringe at on a regular basis. Why go through all of the hassle of finding someone with great skill and knowledge in financial matters only to make huge investment (or lack thereof) decisions alone? People seem to like to ask questions, but ignore the answers. Why do people people tend to underestimate their need to protect themselves financially? Do you tend to make money decisions on your own, or do you ask questions? What credible person do you ask financial advice from? Do you tend to follow their advice or ignore it? Make a short list of three financially savvy people you would feel comfortable asking financial questions to; that you know has your best interest at heart. Read through the attached article and make a list of financial decisions that adults need to make with their money. Mark the items with a star that you will need to consider within the next year. Categorize these decisions with titles such as insurance, investment, and spending, etc. Try and match the list of the people you trust to help you make financially smart decisions with the type of financial decisions you will consider this upcoming year. Share your decisions with a partner and come up with a suggestion for your partner to examine.

Extension: On a 3x5 card, make a “quick guide” for yourself when making decisions with your money. Use the article to lead you in your financial decision making chart.

SS.912.FL.6.1Describe how individuals vary with respect to their willingness to accept risk and why most people are willing to pay a small cost now if it means they can avoid a possible larger loss later. SS.912.FL.6.2Analyze how judgment regarding risky events is subject to errors because people tend to overestimate the probability of infrequent events, often because they’ve heard of or seen a recent example. SS.912.FL.6.3Describe why people choose different amounts of insurance coverage based on their willingness to accept risk, as well as their occupation, lifestyle, age, financial profile, and the price of insurance.  Check out and download our new student guide to use with this article-based lesson!

Many people in today’s society are earning their income in a “pay per job” market. As of 2016, around twenty to thirty percent of the working age population has earned money outside of a typical salaried or hourly pay job. Why do you think this statistic has increased so much over the years? Now read the Tampa Bay Times article below to discover more about the "gig" economy.

The job industry is thriving with entrepreneurial growth. Uber, Lyft, AirBnB, DoorDash and Postmates are just some of the opportunities that allow individuals to earn money around their own schedules, rather than that of their employer. When individuals earn wages on a “individual contract basis,” what does the worker need to take into account? After reading the article below, consider: How has technology changed the job market? Are technological changes helping or hurting the job market? As a student looking for a part time job, free-lance work or gigging may be great opportunities. Create a resume of your work experience, leadership and current responsibilities that show your marketability for an independent contract job. Investigate your earning with a gig job and compare to a local fast-food restaurant’s hourly wage. What can you find out?

Extension: Act as employer and write an ad for a job in a “gig economy.” Make sure to identify both the job qualifications and the personal qualities you need in your employee. Florida Financial Literacy Standards: SS.912.FL.1.1 Discuss that people choose jobs or careers for which they are qualified based on non-income factors, such as job satisfaction, independence, risk, family, or location. SS.912.FL.1.2 Explain that people vary in their willingness to obtain more education or training because these decisions involve incurring immediate costs to obtain possible future benefits. Describe how discounting the future benefits of education and training may lead some people to pass up potentially high rates of return that more education and training may offer. SS.912.FL.1.3 Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. SS.912.FL.1.5 Discuss reasons why changes in economic conditions or the labor market can cause changes in a worker’s income or may cause unemployment. Florida Economics Standards: SS.912.E.1.9 Describe how the earnings of workers are determined.  Check out our new student guide to use with this article-based lesson!

Keep Your Lips Zipped When You Shop! When is the last time you have been on a car lot? Have you flipped through an Automobile Sales Flyer or scrolled online to find your dream car? Did you know that what you say “can, and will be held against you?” There are five topics you must tame your tongue to avoid! Before reading the article, 5 things not to say when you're buying a car, come up with a quick list of items that you may not want to share with a car salesperson. Compare it to the list in the article below.

Part of the battle in purchasing a car is comparison shopping to ensure you are making the best decision. You must weigh information about each vehicle in comparison to each other. Think about such items as price, affordability, auto features, repair costs and your own intention for use and need to a vehicle. Read the article attached and write a short response illuminating the consequences of purchasing a vehicle that just meets or exceeds your price range. What are the consequences to this? Does this affect anyone other than yourself; how so?

Extension: Explore the laws and institutions provided for consumers to help gain adequate information about vehicles. Make a brochure to identify and explain these laws and institutions to another consumer. Florida Financial Literacy Standards: SS.912.FL.2.1 Compare consumer decisions as they are influenced by the price of a good or service, the price of alternatives, and the consumers income as well as his or her preferences. SS.912.FL.2.2 Analyze situations in which when people consume goods and services, their consumption can have positive and negative effects on others. SS.912.FL.2.3 Discuss that when buying a good, consumers may consider various aspects of the product including the product’s features. Explain why for goods that last for a longer period of time, the consumer should consider the product’s durability and maintenance costs. SS.912.FL.2.5 Discuss ways people incur costs and realize benefits when searching for information related to their purchases of goods and services and describe how the amount of information people should gather depends on the benefits and costs of the information. SS.912.FL.2.7 Examine governments establishing laws and institutions to provide consumers with information about goods or services being purchased and to protect consumers from fraud.  Check out and download our new student guide for this lesson!

Unnerving university loans have students second guessing college Taking a risk by going to college and investing in yourself can be scary. Many students take out loans to get through their university experience. The career that they land as a result of furthering their education may or may not pay the bills for the debt. New college grads are finding that taking out loans for college does not always “pay" as illustrated in the Cartoons for the Classroom activity from the Tampa Bay Times Newspaper in Education.

Consider your future career choice and if a degree is needed. What does the average pay look like for your career in the town you would like to work? What is the demand for the career itself? Is there a high occupational outlook? Be sure to weigh the choices in fields where a university education is not needed. If you can work your way through college, even taking an extra year or two- you may be able to graduate without school loans. Depending on the repayment structure for your college loan, it may be years before you pay off any of the principal. What have you heard about college debt? Is it worth it? Search for a “Student Loan Calculator” online. <https://www.bankrate.com/calculators/college-planning/loan-calculator.aspx> Find out how much it costs to take out a loan for $5,000, $10,000 and $50,000 over a 10 year period of time. Create a grid that shows the payments for each with 4%, 5% and 6% interest rates. What would it look like if you take 20 years to pay off your loans? What are the consequences of not paying these loans in a timely manner? What if you miss a payment? Write a paragraph to explain the best choice for you, make sure to explain why.

For more https://www.econedlink.org/resources/how-will-i-pay-for-college/ Extension: Research your chosen career in a specific town and compare the pay to cost of living. Create a budget and find out how much money you have available and are willing to put towards student loans. Florida Financial Literacy Standards: SS.912.FL.4.1 Discuss ways that consumers can compare the cost of credit by using the annual percentage rate (APR), initial fees charged, and fees charged for late payment or missed payments. SS.912.FL.4.8 Examine the fact that failure to repay a loan has significant consequences for borrowers such as negative entries on their credit report, repossession of property (collateral), garnishment of wages, and the inability to obtain loans in the future. SS.912.FL.4.9 Explain that consumers who have difficulty repaying debt can seek assistance through credit counseling services and by negotiating directly with creditors.  Investment News recently stated there is a financial literacy crisis, with an article: Financial Literacy an Epic Fail in America. What can we do to solve the problem?

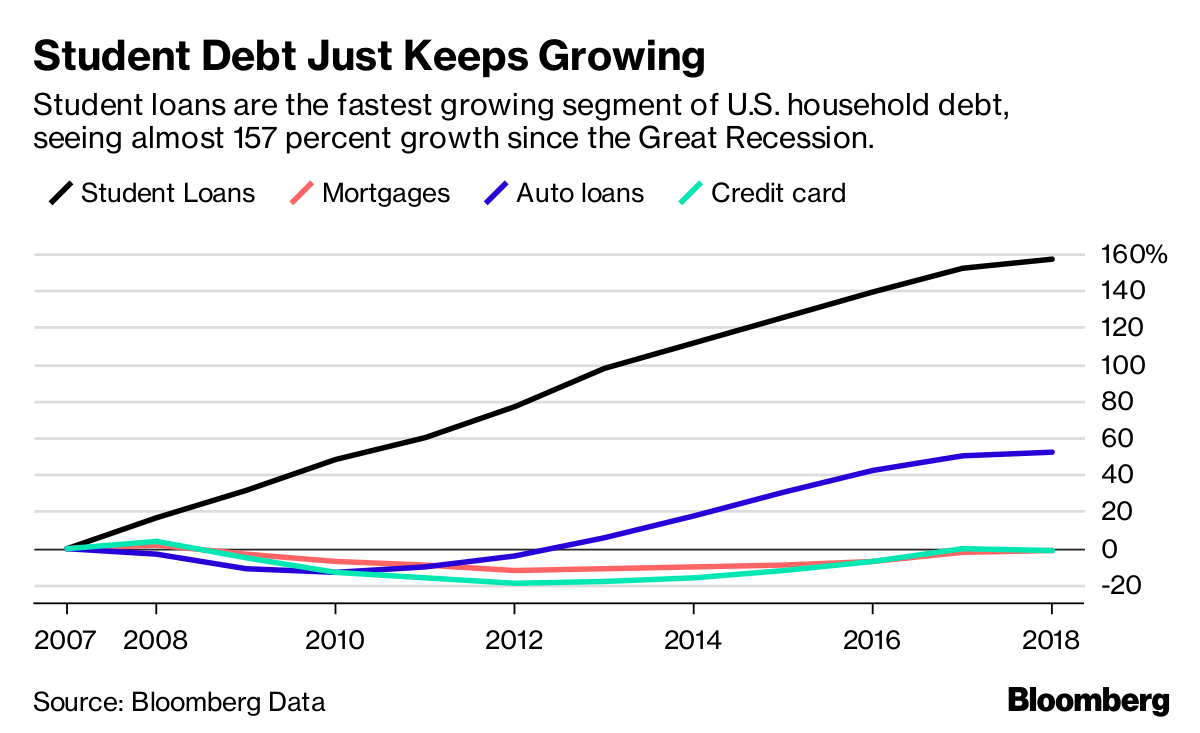

According to the Tampa Bay Times, there is currently legislation that would require a course on financial literacy. If Senate Bill 114 passes, high school students will be required to take a half-credit course as part of their graduation requirements. Named in memory of the late state senator, the Dorothy L. Hukill Financial literacy Act will require this course that will help students learn about money matters that will help prepare them for adulting. What do you think? Conduct some research and then create a social media post during April to celebrate Financial Literacy Month!  As illustrated in the Bloomberg graph above, student loans are the fastest growing area of household debt. And they just keep growing. In the Tampa Bay Times article below, the title reads: Student loan default can gut your paycheck. What do you think that means? Read the article and discuss the consequences of defaulting on a debt. Discuss the costs and benefits of taking out student loans. For more information, check out the information on student loans from the US Department of Education (DOE) .

Financial Literacy Standards

SS.8.FL.1.6 Identify the opportunity costs that education, training, and development of job skills have in the terms of time, effort, and money. SS.912.FL.1.3 Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices.  This photo from the Tampa Bay Times shows a scene from a charity event hosted by the SPCA where they sold dog wedding packages to raise money for a pet shelter in Largo. Why would people be more willing to spend money on a dog wedding if they knew the money was going to charity? Read the article to learn more about the event. Then think of a creative way you could raise money for a favorite charity.

Financial Literacy Standards

SS.912.FL.2.6 Explain that people may choose to donate money to charitable organizations and other not-for-profits because they gain satisfaction from donating. ......  You have probably heard about the growing economy in the news. Does that mean that all families are doing better? Check out the article below from the Tampa Bay Times, entitled: In a Good Economy Report Reveals Grim News for Florida Families. Based on the title, what do you think this article will be about? Why do you think there is "grim news" for some Florida Families? Now read the article. What are some of the problems families are facing? Think about your financial future. Conduct some online research to help prepare for a better financial future. Chances are, you will not have the same job for your entire life. In addition, skills will change over time. What are some decisions people can make to improve their future income?

Financial Literacy Standards

SS.8.FL.1.2 Identify the many decisions people must make over a lifetime about their education, jobs, and careers that affect their incomes and job opportunities. SS.8.FL.1.4 Examine the fact that people with less education and fewer job skills tend to earn lower incomes than people with more education and greater job skills. SS.912.FL.1.3 Evaluate ways people can make more informed education, job, or career decisions by evaluating the benefits and costs of different choices. |

Archives

January 2022

Categories

AuthorDeborah Kozdras, Ph.D. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSS Feed

RSS Feed